A Solo 401k Contribution System That Actually Fits Variable Income

You know the limits. Here’s one way to think about executing them.

A W2 401k contribution requires exactly one decision: how much to defer. Everything else - timing, calculation, execution - happens automatically. The math is done before you see the money. You never have to think about it.

A Solo 401k requires all of it. You are the payroll department. There is no automatic deduction, no employer system doing the calculation, no nudge when a contribution should happen. When a client payment lands in your account, nothing happens next unless you make it happen.

The intuitive response is to wait - until the year is closed, until the numbers are clear, until January. That works in a compliance sense. But it means months of uninvested cash sitting outside the account, compounding nowhere. There is a system worth considering that does better.

The W2 Mindset May Be the Wrong Model

A W2 contribution is triggered by a payroll cycle. A Solo 401k contribution can be triggered by a client payment instead.

Every time a consulting payment arrives, you have everything you need to calculate how much to contribute - for that payment, based on that income. The formula is the same every time. You don’t need to know your full year income. You don’t need to wait for a calendar event.

The calculation for each payment:

Payment received minus business expenses attributable to that payment = net profit

Net profit × 92.35% × 15.3% ÷ 2 = half SE tax deduction

Net profit minus half SE tax deduction = adjusted net income for that payment

Adjusted net SE income × 20% = employer profit sharing contribution

Remainder of adjusted net SE income (up to your running ceiling) = voluntary after-tax mega backdoor contribution

Run this on every payment. Contribute. Update your running tally. Repeat.

The One Problem With Per-Payment Contributions

The formula works cleanly as long as your business expenses are known. The risk: a business expense that arrives after a payment has already been processed - a late invoice, an annual renewal, an unexpected cost - reduces your true adjusted net income for the year without a corresponding payment to deduct it from. If you’ve already contributed based on higher net income, you’ve over-contributed. Over-contributions trigger a 10% excise tax on the excess.

A practical fix: front-loading.

At the start of the year, inventory every known annual business expense - software subscriptions, professional memberships, equipment, insurance, anything you can anticipate. Count the entire year’s expected expenses against your first payment, or your first two if the first isn’t large enough to absorb them all. And you can overestimate to be conservative. For example, if you expect $4,000 in annual expenses, count $5,000 against the first payment.

Once the full year’s estimated expenses are counted upfront, every subsequent payment is pure net profit. No expense uncertainty hanging over the calculation. The formula stays clean for the rest of the year.

The overestimate creates a small gap between your in-year contributions and your actual adjusted net income ceiling. That gap gets settled in January - once the year is closed and your final Schedule C is confirmed - as a true-up contribution. Note that your plan provider may have administrative deadlines earlier than the statutory deadline of April 15 (October 15 with extension) - confirm your provider’s cutoff before assuming the full window is available. A small January contribution is a feature, not a problem. It means you contributed conservatively during the year and have a clean final number to work from.

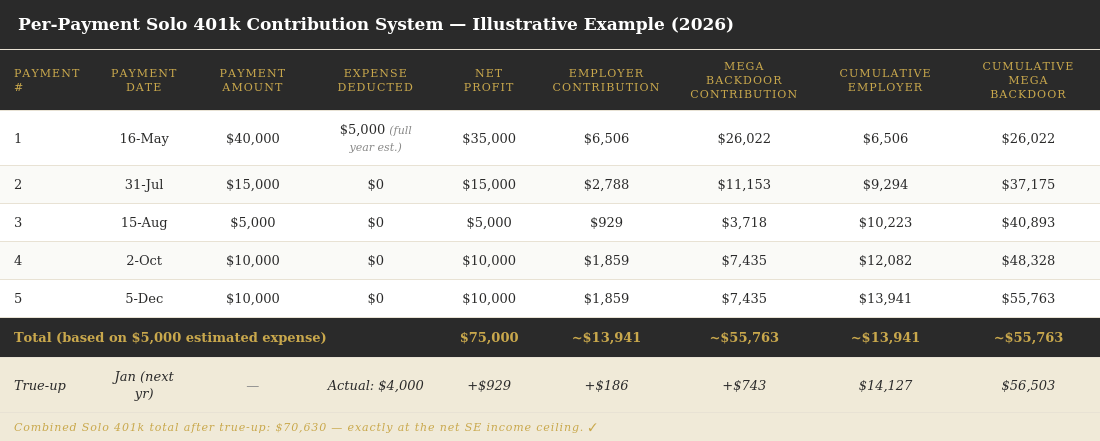

What This Might Look Like in Practice

The table below illustrates the per-payment system applied to five client payments across a year. It tracks each payment from receipt to contribution, with expenses front-loaded against Payment 1 at the estimated annual amount. Every subsequent payment runs through the same formula on pure net profit. The cumulative columns show the running total against the $70,630 ceiling.

By December the contributions are done - fully deployed, fully invested, no year-end scramble. The true-up row shows what happens in January when actual expenses ($4,000) come in below the estimate ($5,000). The $1,000 difference unlocks a small additional contribution that closes the gap exactly at the ceiling.

The table assumes the full available contribution room goes into the Solo 401k at each payment - the maximum deployment scenario. In practice you may want to retain some of the mega backdoor room for personal expenses, savings, or liquidity. The system works the same way either way - you simply contribute less than the full calculated amount at each payment, and the January true-up handles whatever room remains.

What This Actually Changes

The difference between contributing per payment versus waiting until January for a single lump sum is compounding. Money contributed in May has eight months of additional growth before the January true-up. Money that sits in a bank account waiting for year-end reconciliation does not. On the contribution amounts in the example above, at a 10% annual return, a per-payment approach generates roughly $3,000 in additional growth in that first year alone. Compounded over a decade of consulting income, the gap is meaningful.

A per-payment system is not complicated. It requires one spreadsheet, one formula, and the discipline to run the calculation every time a payment arrives rather than filing it away for later.

The W2 never required that discipline because it never needed to. The Solo 401k is a different game.

I am not a financial advisor or tax advisor. Nothing in this newsletter is investment or tax advice. Contribution limits and calculations illustrated here are for educational purposes and reflect 2026 limits. Consult a qualified CPA or professional before making contribution decisions. Fine Print Investing publishes weekly.