The Fine Print Nobody Reads

A few years ago I invested a significant amount of money into a real estate deal that looked perfect on paper.

I did the work. Researched the location. Studied the local market. Analyzed the economic fundamentals. The pro forma was solid. Every number pointed in the right direction. I felt good about it.

It failed. Badly.

Not because the market was wrong. Not because my analysis was off. The asset was fine. The management team wasn’t. They were inexperienced, in over their heads, and - I realized too late - much better at raising capital than actually running a property. The books teach you how to analyze a pro forma. Almost none of them teach you how to assess whether the people you’re handing your money to actually know what they’re doing. That’s the fine print that determines whether a deal lives or dies. And I learned it the hard way.

That experience changed what I look for in a deal. I still run the numbers. But now I spend just as much time on the people behind them.

I am genuinely addicted to personal finance content - books, blogs, podcasts, random Substack newsletters from people I’ve never heard of. I consume it constantly. My wife has stopped asking what I’m reading because the answer is always some variation of “a book about money.”

But the more I read, the more something started bothering me. Because after a while you notice - it’s the same stuff, recycled endlessly. Nobody stops to check if any of it is actually true. Wake up at 5am. W2 is a dead end. Everyone should buy rental properties. Crypto is the future. Each idea delivered with the absolute certainty of someone who has never once asked whether it applies to your specific life, your income, your actual circumstances.

Here’s what drives me crazy: the upside always gets the headline. The fine print - the risks, the caveats, the conditions under which any of this actually works - gets the footnote, if it shows up at all.

Last month I saw a post from someone who “retired” at 38. Half a million followers. Comments full of people asking how they could do the same. What the post didn’t mention: he still runs a podcast, sells a course, does paid speaking, and consults on the side. That’s not retirement. That’s a career pivot with better branding. And nobody in the comments was asking about it.

That’s the pattern. The headline is simple and inspiring. The fine print - the part that actually determines whether the idea works for you - gets mysteriously skipped. Because fine print doesn’t go viral. Caveats don’t sell courses. And most of the people teaching this stuff have probably never actually put their own money on the line. They read something for thirty seconds, repackaged it, and now they’re the expert. I don’t care what you preach if you haven’t done the work, made the mistakes, and lost real money trying. If you lost money and learned something honest from it - okay, now I’m listening. That’s actually useful. The rest of it is just noise with good lighting.

I have a PhD in a quantitative field. Fifteen years as a consulting executive. My job, literally, is to look at messy data and find what’s actually true. I’ve sat across enough confident but completely wrong people to know what BS looks like up close. I know it fast.

And I’ve put my own money on the line. The real estate syndication above is one example. There are others - some that worked, some that didn’t. The ones that didn’t taught me more. Mostly they taught me to read the fine print before I wire the money.

What I do have is zero hesitation calling BS when I see it.

So what is this newsletter?

It’s me sharing what I’ve actually learned along the way. Working through ideas in public. Asking the questions the smiling, confident internet gurus tend to skip: Is this actually true? True for whom? Under what conditions does this work, and when does it fall apart? Who benefits from me believing this? Did the person saying it actually do it - or are they just really good at talking about it?

I’m not a financial advisor. I don’t have a portfolio returning 300% annually - and if you’ve been on Substack for ten minutes today you’ve already met someone claiming they do. I don’t have all the answers. I’m still figuring things out myself, and I’ll tell you when I’m wrong.

I write for people like me. Busy, analytical, probably earning good money - but frustrated that most financial advice feels like it was written for someone else. People who, when they read that early retirement post, felt something was slightly off but couldn’t quite name it.

That’s what this newsletter is for. Every week.

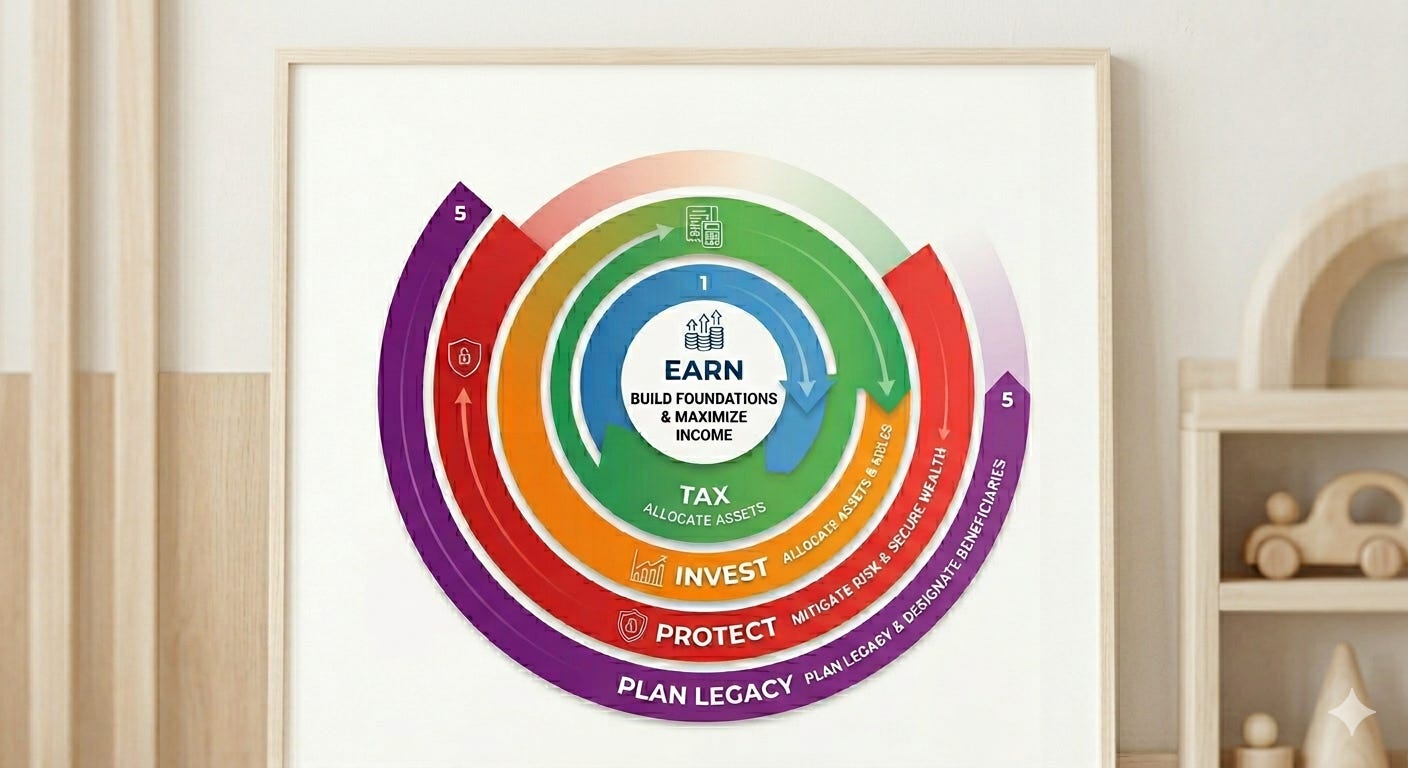

I’ve realized that wealth isn’t just about making money; it’s about managing the interconnected system of your financial life. To do that, I break everything down into five core layers:

Earn is the foundation - not just how much you make, but how it’s structured. Equity compensation, the W2 vs. entrepreneurship decision, side income. The decisions here have tax and wealth consequences that ripple through everything else, often invisibly.

Tax is where high earners leave the most money on the table. Not because they’re careless, but because the standard curriculum stops at “max your 401(k)” and never goes deeper. Which accounts to use, in what order, with what tax treatment - backdoor Roth, mega backdoor, asset location, conversion sequencing. Every dollar saved here is a guaranteed return.

Invest is where capital goes to work. The interesting questions at this income level aren’t usually about which funds to pick - index funds mostly solve that. They’re about which vehicles, in what sequence, with what tax treatment. And they interact constantly with the tax layer, which is why you can’t optimize them in isolation.

Protect is the most underwritten layer on the stack, and the one that can undo everything above it fastest. Disability insurance, umbrella coverage, asset protection structures - the decisions most high earners either skip entirely or never examine with the same rigor they bring to everything else.

Transfer is what happens to the wealth you’ve built. Estate planning, beneficiary designations, the mechanics of passing wealth efficiently across generations. This layer gets deferred until it’s too late to do it well more often than any other. The interactions with the layers above it - Roth conversions as estate tools, asset location with heirs in mind - are where some of the most consequential fine print lives.

The layers matter individually. They matter more together. A gap in tax compounds every year inside invest. A gap in protect can unwind years of careful work in a single event. Most high earners have read enough to be dangerous in one or two layers. Almost nobody has thought carefully about all five, in sequence, as a system.

That’s what we’re building here.

The financial fine print that changes everything is out there. Most people skip it.

We’re going to read every word of it.

Join us to start mastering your system.

Fine Print Investing publishes weekly. Free to start. If this resonated , leave a comment. I read everything.