W2 and a Side Business: How Much Can You Actually Put Away?

Most people with two income streams assume one set of retirement contribution limits. There are actually two - and the difference is significant.

I found myself running numbers on my friend’s situation recently. She has a W2 job and a coaching practice that’s been generating real income for about six months now. With about ten years to retirement, she’s thinking hard about how to make every dollar count. She’s paid off her house, paid off everything really - but her kid is in college and the tuition bills are real, which means she needs to think carefully about how much of her income she can actually deploy into retirement savings right now versus in two years when the college bills stop.

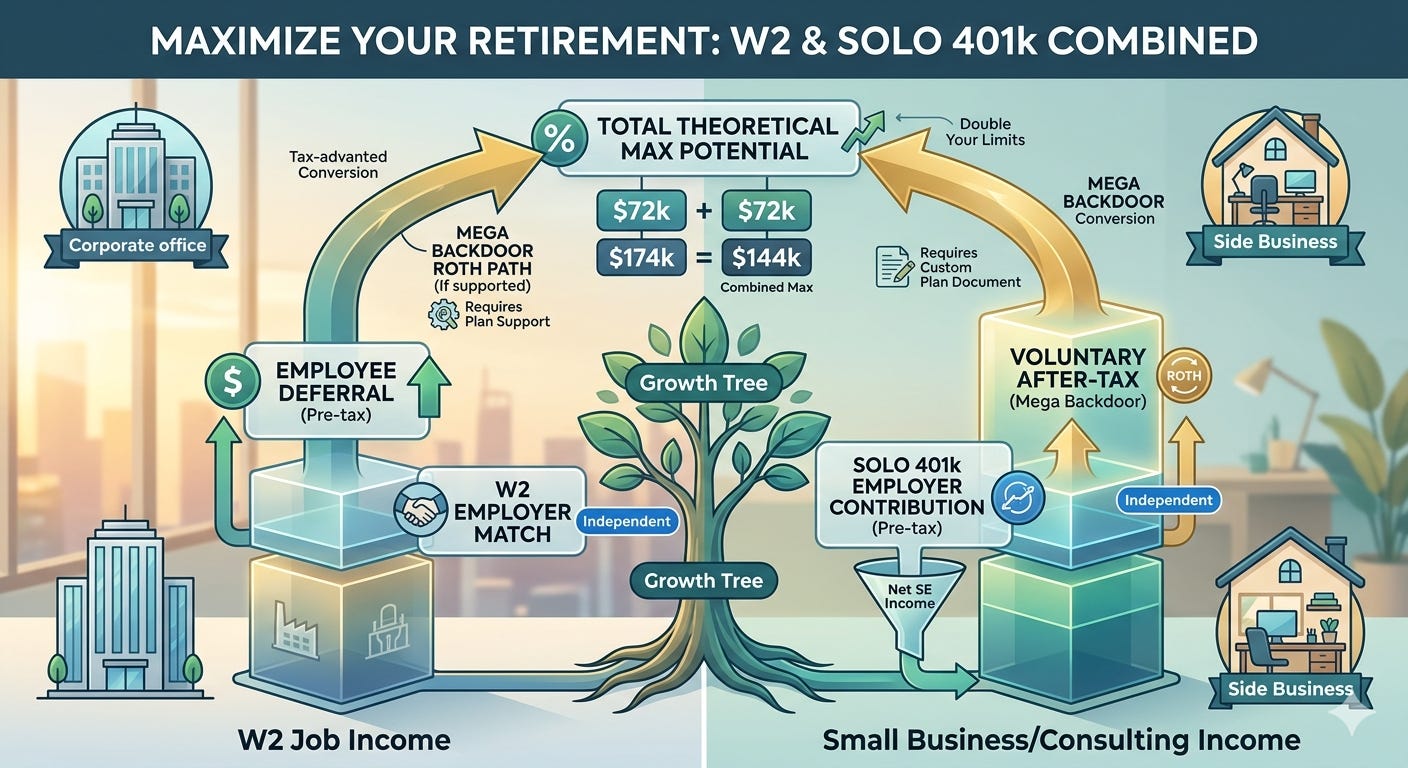

Here’s what most people with a side business don’t know: whether or not your W2 plan offers mega backdoor Roth has nothing to do with whether you can access it. A properly set up Solo 401k unlocks it independently. The two plans operate on completely separate ceilings.

But those ceilings aren’t simply $72,000 each. The Solo 401k ceiling is determined by your adjusted net income - not by what the IRS allows on paper or what the business generates after income taxes. That distinction matters more than most people realize, and it’s where the math gets interesting.

And the reason it’s interesting comes down to one distinction almost nobody explains clearly: some retirement contribution limits are per person, and some are per plan. Getting that distinction wrong is what leads people with two income streams to leave significant tax-advantaged space on the table.

If you haven’t read the prior post on Solo 401k basics, start there. This post picks up where that one left off - with the math.

The Bucket Structure

Every 401k plan - W2 or Solo - has three potential contribution buckets.

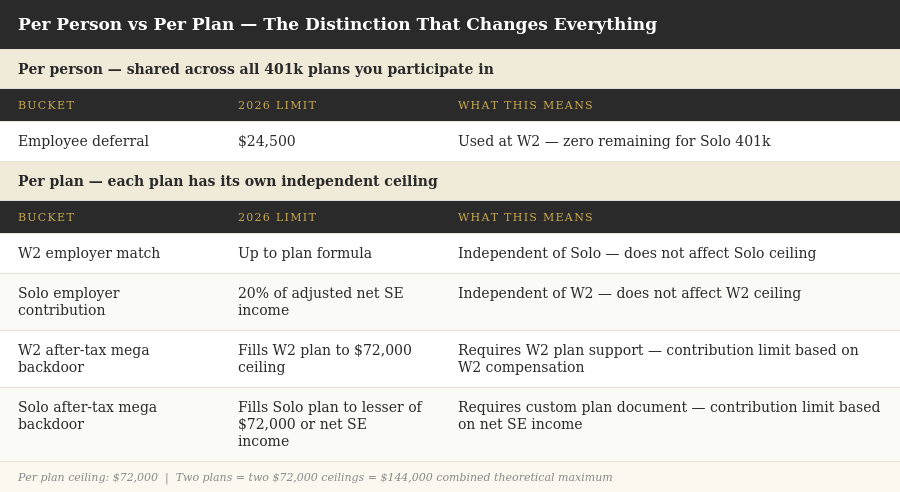

The first is the employee deferral. This is the $24,500 you contribute from your own paycheck in 2026. This limit is per person across all plans. If you max it at your W2 job, you cannot contribute another $24,500 to your Solo 401k on top of that. One pool, shared across every plan you participate in.

The second is the employer contribution. For a W2 plan this is whatever your employer matches. For a Solo 401k this is up to 20% of your adjusted net income - you contribute this as the employer side of your own business. This limit is per plan. Your W2 employer’s match and your Solo 401k employer contribution are completely separate. Both are available simultaneously regardless of what the other plan does.

The third is the voluntary after-tax contribution. This is money contributed beyond the employee deferral using after-tax dollars. Once inside the plan, those after-tax contributions can be converted to Roth - that conversion is what people refer to as the mega backdoor Roth. This limit is also per plan. Each plan has its own ceiling. On the Solo 401k side it requires a custom plan document - the standard brokerage version doesn’t support it, as covered in the prior post.

The total limit across all three buckets is $72,000 per plan in 2026, or 100% of adjusted net income, whichever is less.

One rule worth stating clearly before the scenarios: you cannot cross-contribute between plans. Solo 401k contributions must be based on self-employment income — the contribution amount cannot exceed what the business generates in adjusted net income. W2 mega backdoor contributions must be based on W2 compensation. The funds themselves can technically come from any account, but the contribution limit is determined by each plan’s own income source.

Her Numbers

To make the scenarios concrete, here are the inputs:

W2 salary: $250,000. W2 employer match: 50% of contributions up to 6% of salary = $7,500. All employee deferrals pre-tax. For illustrative purposes, assume she files taxes as a single filer.

Consulting gross revenue: $80,000. Business expenses (5%): $4,000. Net profit: $76,000.

SE tax on $76,000 is approximately $10,740. After deducting half of that ($5,370), the adjusted net income is approximately $70,630. The Solo 401k employer contribution is 20% of that figure, or approximately $14,000.

The total Solo 401k ceiling is the lesser of $72,000 or adjusted net income - in her case approximately $70,630. After the $14,000 employer contribution, the remaining room for voluntary after-tax contributions is approximately $56,600. That is the mega backdoor ceiling on the Solo 401k side. Note that this ceiling is set by the contribution math, not by after-tax cash flow. The income tax on the consulting income is a separate obligation. In her case it is funded comfortably from W2 take-home. But the two numbers are distinct: the contribution ceiling and the tax bill are not the same thing.

Scenario 1 - The Standard Setup

Max the W2 employee deferral, capture the employer match, add the Solo 401k employer contribution from consulting income. No after-tax contributions on either side.

Combined total: ~$46,000. Many people with both income streams never set up a Solo 401k at all - for them the ceiling is just $32,000 from the W2. Those who do set one up often stop at the employer contribution. The after-tax mega backdoor on the Solo side is the layer that goes unused.

Scenario 2 - Solo Optimized

Same W2 setup. Add the Solo 401k mega backdoor using the full available after-tax contribution room.

The voluntary after-tax ceiling on the Solo 401k is approximately $56,600 - the gap between the $70,630 adjusted net income ceiling and the $14,000 employer profit sharing contribution already made. Those funds go directly into Roth accounts via in-plan conversion. The income tax on the consulting income is funded separately from W2 take-home, which at approximately $153,000 after taxes covers both living expenses and the tax obligation comfortably.

Combined total: approximately $102,600 annually in tax-advantaged contributions — roughly $56,600 more than Scenario 1, with the incremental amount entirely in Roth accounts that won’t be taxed again at withdrawal.

This is where my friend lands right now. Her kid is in college and the tuition is real. The W2 take-home covers her life comfortably including the college bills and the consulting income tax bill. The consulting income she’s happy to funnel entirely into retirement savings. Scenario 2 fits her situation precisely: aggressive retirement building without compressing the lifestyle her W2 income funds.

Scenario 3 - Maximum Configuration

Two important assumptions underpin this scenario. First, the W2 plan must support after-tax contributions and in-plan Roth conversions - as covered in an earlier post, only about 22% of employer plans offer this. Second, the $40,000 W2 after-tax figure assumes the $7,500 employer match is the only employer contribution - plans with additional profit sharing would have less after-tax space available.

With those conditions met, add the W2 mega backdoor on top of Scenario 2. Combined total: approximately $142,600. On a $250,000 salary, after taxes a single filer takes home roughly $153,000. Deploying $40,000 of that into after-tax W2 contributions leaves about $113,000 for living expenses. With college tuition in the picture that is tight - manageable, but tight.

The path to Scenario 3 is visible from where she sits. In two years the kid graduates. The college bills stop. The $40,000 W2 mega backdoor that felt uncomfortable becomes straightforward. And if the coaching practice grows - more clients, higher rates, a practice generating $150,000 or $200,000 instead of $80,000 - the Solo 401k after-tax ceiling rises with it, potentially approaching the full $72,000 contribution cap. Someone with lower fixed expenses or a stronger savings cushion might go straight to Scenario 3 today. The lifestyle calculus is personal.

What This Adds Up To

The difference between Scenario 1 and Scenario 2 is approximately $56,600 annually going into Roth accounts. Between Scenario 1 and Scenario 3 it’s approximately $96,600. On identical income. The only variables are the plan documents and the cash flow to fund them.

The reason people miss Scenario 2 isn’t the contribution limit mechanics - it’s not knowing that a custom Solo 401k plan document unlocks mega backdoor Roth access even when the W2 plan doesn’t offer it, and not realizing that the Solo 401k contribution ceiling is set by adjusted net income, not by after-tax cash. Someone whose W2 plan has no mega backdoor option can still access it through the Solo 401k.

If you have both income streams and haven’t had this conversation with your CPA, now you know what to ask.

Have you run these numbers for your own situation? Leave a comment - I’m curious where people land and whether Scenario 2 or 3 is realistic given your income and expenses.

I am not a financial advisor or tax advisor. Nothing in this newsletter is investment or tax advice. Contribution limits, tax rates, and calculations illustrated here are for educational purposes and reflect 2026 IRS limits. Consult a qualified CPA or ERISA attorney before making contribution decisions. Fine Print Investing publishes weekly.